A Defense Tech Market Map

A Defense Tech Market Map

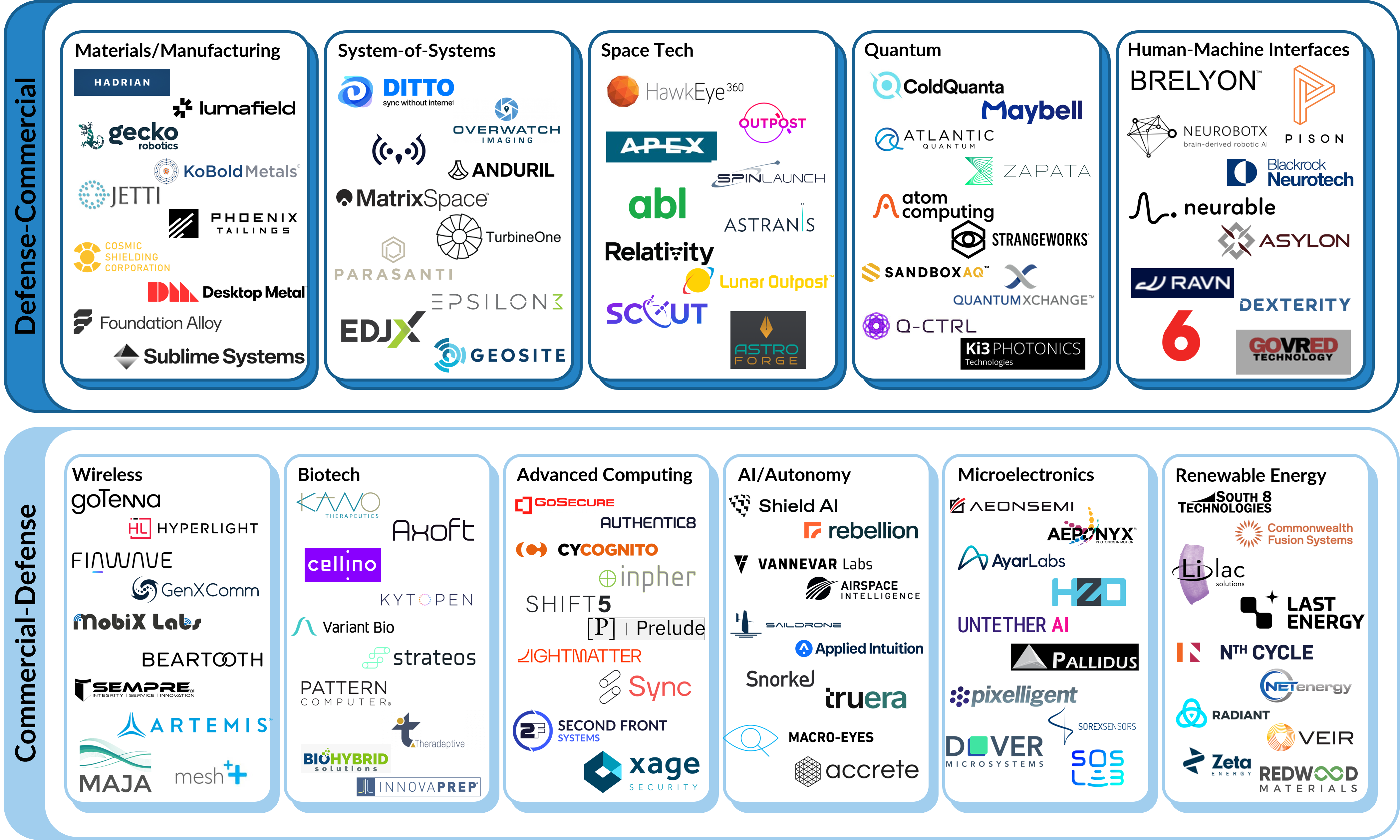

Let's start with an overview of the Defense Tech Ecosystem!

Much has been written about both the importance of investing in defense technology and the challenges of investing in and fielding innovative technological capabilities in the national security space. I won’t take too much time highlighting the context beyond echoing some truisms:

Maintaining technological competitiveness in key innovation challenges is paramount to preserving America’s position relative to adversaries and succeeding in 21st century conflict

Innovation—and effective adoption of innovation—is stymied by a series of structural challenges not limited to innovation theatre-ism, byzantine processes, poor incentive alignment, etc.

That all being said, “government is bad at innovation” isn’t a winning or actionable strategy, and successful adoption of innovation requires active participation from government and shared vision/leadership from public and private sector stakeholders (maybe more on this another time)

Investment in dual-use and defense technologies from the private sector and private capital markets is a critical tool to driving innovation and countering adversarial systems like China’s civil-military fusion

For the purpose of this piece, I want to focus on unpacking the last bullet-point (in context of the prior 3): What does the startup ecosystem look like today and how does it map onto what is required to identify and field innovative capabilities? To answer this, I’ve pulled together a market map that highlights archetypical innovators within priority areas for dual-use and defense technology. This is by no means a comprehensive guide to every startup building a dual-use or defense capability but is instead meant to illustrate major themes and subgroups of startups within priority technology areas for the DoD.

I followed two major organizing frameworks in creating this market map. First, I broadly split the technologies into one of two groups from Jake Chapman’s piece in War on the Rocks from September 2022. In the article, Chapman breaks down defense technology into 4 major groups: Defense-Defense (things that originate in Defense and stay there), Commercial-Commercial (commercial COTS/GOTS products), Defense-Commercial (Defense-born technologies that may achieve commercial use cases and scale), and Commercial-Defense (classic dual-use technologies that start commercial first and move to Defense).

I believe this framework is useful because it provides a intuitive understanding of the acquisition environments and challenges that mark the technologies’ path to market. Defense-Defense tech will likely come from large OEMs and primes while Commercial-Commercial is likely to be enterprise software. The two mixed-categories are the more interesting focal point: Defense-Commercial technology may have more technical risk, be more R&D-heavy, or come from sources like federal R&D spin-out. Commercial-Defense will hit the commercial market first—requiring viable commercial scale before pursuing a Defense market-- something Chapman highlights as problematic since the product-market fit may not be there and the defense market is deprioritized. For the dual-use market map, I focused on technologies that fell into these latter two buckets.

On top of this, I overlayed—somewhat imperfectly—the 14 technology areas identified by the Undersecretary of Defense for Research & Engineering. Three areas—directed energy, hypersonics, and integrated sensing & cyber—fell into the Defense-Defense bucket and weren’t included in the market map. These technologies may have commercial ventures but innovation in this space may mostly be led by DoD stakeholders rather than the commercial sector. The other 11 priority areas were mapped onto Commercial-Defense or Defense-Commercial buckets.

While many other classifications for technology areas may be more precise at classifying startups within this space—and while startups may actually fit into multiple categories below—I think the USD(R&E) mapping is important with regard to bullet 3 above. Commercial sector innovators have to be able to speak DoD language to navigate the space effectively. Understanding how a commercial venture’s product maps onto the DoD’s priorities is critical to gaining effective adoption. So, while imperfect—I think this mishmashed framework can highlight how technology can find its way to deployable capability:

Big takeaway for me here is the breadth and depth of the technologies that are relevant in the dual-use space. Investors in dual-use and defense tech and best served finding niches within these segments rather than chewing off “defense tech” as an investment thesis. For example, within Renewable Energy there’s several subsegments from battery technology, to renewable energy and nuclear, to energy generation, storage, transmission, recycling, etc. that would benefit from technically-savvy investors who understand the minutia of the space.

That being said, I think viewing the Defense market in context of its totality is an important point of view for investors to understand how technology can transcend across segments and how the totality of DoD spend in this area interacts. Quantum and Biotech for example may see strong synergies on new methods of drug discovery, testing, and simulation. Wireless, System Tech, AI, and Advanced Computing all interact to form integrated, secure, and intelligent communications systems. And so, growth in these areas will be crowded in, creating economies of scale and investment opportunities at the interaction points.

Next time, I’ll hope to put some numbers behind this to add some credence to the mission and opportunity within the dual-use tech space. Then, we’ll unpack each box, diving deep into the market, trends, movers & shakers, to glean insights on investing in dual-use technology. But for now, let me know: what am I missing? What can be better?